RRSP Explained: Stop Overpaying CRA — The Smart RRSP Tax Strategy to Get Thousands in Tax Refunds Today, Grow Your Investments Tax-Free, and Pay Less in Retirement, with RRSP Contribution Tax Refund Strategy,

RRSP Contribution Tax Refund: Reduce Your 2026 Taxes and Increase Your Refund

If you are earning employment or business income in Canada, understanding your RRSP contribution tax refund opportunity could save you thousands of dollars this tax season. Every year, many Canadians miss the full benefit of their RRSP contribution, either because they wait until the last minute or they do not understand how RRSP tax savings truly work. With the upcoming RRSP deadline for the 2025 tax year approaching in early March 2026, now is the time to plan strategically — not reactively.

Let’s break down how an RRSP contribution tax refund works and how you can use it as a long-term planning strategy.

What Is an RRSP Contribution Tax Refund?

An RRSP contribution tax refund happens when your RRSP contribution reduces your taxable income, resulting in lower taxes payable — and often a refund. When you make an RRSP contribution, you receive an RRSP tax deduction.

That deduction reduces your taxable income.

Lower taxable income = lower tax liability. If tax was already deducted from your paycheque, you may receive an RRSP tax refund when you file your return. This is one of the most powerful RRSP benefits available to Canadian taxpayers.

RRSP Contribution Tax Refund: How to Reduce Taxes Today and Pay Less in Retirement

An RRSP contribution tax refund occurs when your RRSP contribution reduces your taxable income and lowers the amount of tax you owe. When you make an RRSP contribution, you receive an RRSP tax deduction, which reduces your income dollar-for-dollar. For example, if you earn $120,000 and contribute $20,000 before the RRSP deadline, your taxable income drops to $100,000. Because income tax in Canada is calculated using marginal tax brackets, this reduction can generate a significant RRSP tax refund when you file your return.

The higher your marginal tax rate, the larger your RRSP tax savings. This is why RRSP contribution tax refund planning is especially valuable for professionals, business owners, and higher-income earners.

RRSP Withdrawal Tax and Paying Less in Retirement

Yes, RRSP withdrawal tax applies when you withdraw funds. However, the strategy behind an RRSP contribution tax refund is tax deferral — not tax elimination. You contribute when your income and tax rate are higher. You withdraw later when your income may be lower.

If you contributed at a 43% tax rate and withdraw in retirement at 20–25%, you effectively shifted taxation from a high bracket to a lower one. This bracket management is how RRSP tax planning reduces lifetime taxes. This is also where comparing RRSP vs TFSA becomes important. RRSP is generally more beneficial when you are in a higher tax bracket and expect lower income later.

RRSP Contribution vs TFSA: Which Strategy Is Better?

When comparing RRSP vs TFSA, the answer depends on income level and financial goals.

RRSP is typically better when:

- You want an immediate RRSP contribution tax refund

- You are in a high marginal tax bracket

- You want structured retirement income planning

TFSA may be better when:

- Your current income is low

- You expect higher income in the future

- You need flexible withdrawals without tax consequences

A proper long-term planning strategy evaluates both options rather than choosing blindly.

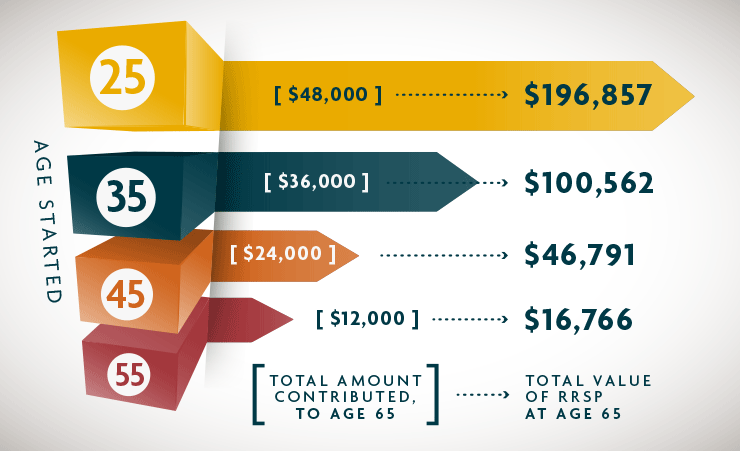

How RRSP Tax Savings Grow Over 25 Years

An RRSP contribution tax refund provides immediate tax savings, but the long-term RRSP benefits are equally powerful. Investments inside an RRSP grow tax-deferred. This means you do not pay annual tax on interest, dividends, or capital gains while the funds remain inside the plan. For example:

- RRSP contribution: $20,000

- Average annual return: 5%

- Investment period: 25 years

After 25 years, the investment could grow to approximately $67,800. Because the investment growth is sheltered from annual taxation, compounding works more efficiently compared to investing in a taxable account. This is why RRSP tax savings are not just about a refund today — they are part of a structured long-term planning strategy.

Why the RRSP Deadline Is Important for Maximizing Your Tax Refund

The RRSP deadline is typically 60 days after December 31 of the tax year. For the 2025 tax year, the RRSP deadline will generally fall around early March 2026 (subject to confirmation by the Canada Revenue Agency).

Missing the RRSP deadline means you lose the opportunity to claim your RRSP tax deduction for that tax year — which also means losing your RRSP contribution tax refund for that period. Planning your RRSP contribution before the deadline allows you to:

- Reduce your current tax bill

- Increase your tax refund

- Improve cash flow

- Align your contribution with a long-term planning strategy

Waiting until the last week before the deadline often results in rushed decisions rather than optimized tax planning.

Frequently Asked Questions (FAQs) About RRSP Contribution Tax Refund

Your RRSP contribution tax refund depends on your marginal tax rate and contribution amount. For example, if you are in a 40% tax bracket and contribute $10,000, your RRSP tax refund could be approximately $4,000. Higher-income earners generally receive larger RRSP tax savings because their tax rate is higher.

The RRSP deadline is generally 60 days after December 31 of the tax year. For the 2025 tax year, the deadline is expected to be around March 2, 2026. Contributions made before this RRSP deadline can be claimed as an RRSP tax deduction for that year.

An RRSP tax deduction reduces your taxable income. If you earn $100,000 and contribute $15,000, your taxable income becomes $85,000. Because tax is calculated on taxable income, your total tax payable decreases, which may result in an RRSP contribution tax refund.

Yes, an RRSP calculator can provide a rough estimate of your RRSP tax refund based on income and contribution amount. However, calculators do not consider all variables such as credits, deductions, or long-term tax strategy. Professional planning ensures more accurate optimization.

If you miss the RRSP deadline, you cannot claim the RRSP tax deduction for that tax year. While your contribution room carries forward, you lose the immediate RRSP contribution tax refund opportunity for that period.

Yes, RRSP withdrawal tax applies to withdrawals. The amount of tax depends on your income level at the time of withdrawal. Many retirees withdraw at a lower tax rate than when they contributed, reducing total lifetime tax.

RRSP provides an immediate tax deduction and potential RRSP contribution tax refund, while TFSA contributions are not deductible but withdrawals are tax-free. Choosing between RRSP vs TFSA depends on your current and expected future tax bracket.

Maximizing your RRSP contribution tax refund requires more than simply making a deposit before the RRSP deadline. It requires structured tax planning, analysis of your marginal tax rate, and a long-term retirement strategy. At VanTax Accounting Services, we provide comprehensive personal tax return filing, corporate tax return preparation, RRSP tax planning, TFSA vs RRSP strategy consultation, retirement tax planning, tax refund optimization, business tax advisory, and long-term tax planning strategies designed to reduce taxes legally and efficiently. Whether you are a salaried professional, self-employed individual, or incorporated business owner, our team helps you align your RRSP contribution, RRSP tax deduction, and future RRSP withdrawal tax planning with your overall financial goals. We proudly serve clients across Vancouver, Burnaby, Coquitlam, Port Coquitlam, Surrey, and the Greater Vancouver area, offering both in-person and virtual consultations. If you want to reduce taxes today, increase your RRSP tax savings, and build a smarter long-term planning strategy, professional guidance can make a measurable difference.

Comprehensive Tax, Accounting, and Business Advisory Services at VanTax

Beyond optimizing your RRSP contribution tax refund, VanTax Accounting Services provides complete support as your trusted tax accountant and bookkeeper. We offer professional bookkeeping services, accurate financial statement preparation, and strategic financial advisory services to help individuals and businesses make informed financial decisions. For growing businesses, we deliver structured corporate tax planning, reliable business tax services, and practical internal audit services designed to improve financial controls and operational efficiency. Our CFO on a contract basis solution gives business owners executive-level financial insight without the cost of a full-time CFO, helping you analyze cash flow, profitability, tax efficiency, and long-term growth opportunities. Serving Vancouver, Burnaby, Coquitlam, Port Coquitlam, Surrey, and the Greater Vancouver area, we support professionals, entrepreneurs, and corporations with integrated tax planning, bookkeeping, financial reporting, and business advisory services — all focused on sustainable business growth and long-term financial stability.